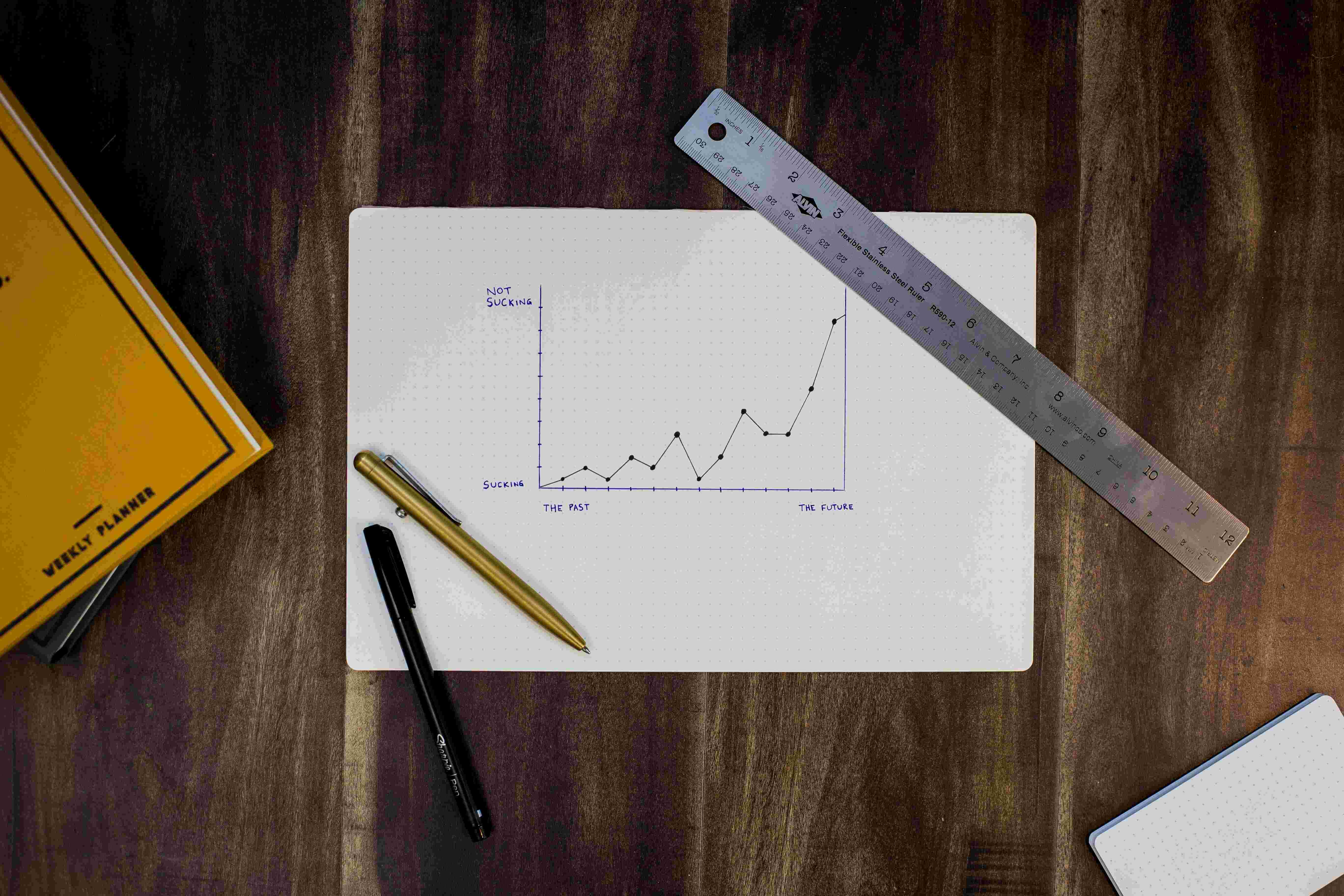

What is Incremental Budgeting?

Incremental budgeting is one of the Types of Budgeting Methods in which an organization creates a new budget based on the previous budget’s figures, making incremental adjustments for changes and developments. It is a budgeting approach that builds upon the existing financial plan, typically by adding or subtracting a fixed percentage or incremental amounts to the previous budget. Incremental budgeting is a common practice in many organizations, as it provides a straightforward and efficient way to create budgets for future periods while considering historical data and performance.

Incremental Budgeting Method

The incremental budgeting method involves making adjustments to a previous budget to create a new budget for the upcoming period. For example, if a department had a budget of $100,000 for office supplies in the previous year and expects a 5% increase in prices and usage for the next year, the incremental budget for office supplies would be $105,000.

Similarly, if another department had a budget of $50,000 for travel expenses in the previous year and intends to reduce travel due to cost-saving measures, the incremental budget might be set at $45,000 for the next year. This method allows organizations to consider changes in expenses while maintaining a degree of consistency with previous budgetary allocations.

How Does Incremental Budgeting Work?

Incremental budgeting works by taking the previous budget as a starting point and making adjustments based on various factors such as inflation, changing business conditions, or specific departmental needs. The process typically involves the following steps:

1. Start with the Previous Budget: Begin with the budget figures from the previous year as the foundation.

2. Identify Changes: Identify any changes or factors that will affect the upcoming budget period. This can include cost increases, reductions, or shifts in priorities.

3. Adjust Line Items: Make incremental adjustments to the line items within the budget to reflect the anticipated changes. These adjustments may involve percentage increases or decreases, fixed-amount changes, or allocation shifts.

4. Review and Approve: Review the adjusted budget and seek approvals as necessary from relevant stakeholders, such as department heads or executives.

5. Implement the Budget: Once approved, the incremental budget becomes the financial plan for the upcoming period.

Advantages of Incremental Budgeting

There are several advantages of incremental budgeting, including simplicity, efficiency, and the ability to build on prior financial plans. It allows organizations to:

– Save time and resources by using existing budget data.

– Maintain a degree of consistency with previous budgetary allocations.

– Focus on key changes and adjustments rather than recreating the entire budget.

– Easily track and analyze changes from the previous budget period.

Disadvantages of Incremental Budgeting

Despite its advantages, there are also some disadvantages of incremental budgeting. A few of the drawbacks include:

1. Potential for budgetary slack: Departments may request incremental increases to their budgets to build cushions, leading to unnecessary spending.

2. Lack of cost-effectiveness: Incremental budgeting may not encourage a thorough review of all expenses, potentially missing opportunities for cost savings.

3. Limited consideration of new priorities: It may not adequately address emerging needs or shifting strategic priorities, as it primarily relies on historical data.

4. Difficulty in justifying allocations: Incremental changes may not be well-justified, making it challenging to defend budgetary decisions to stakeholders.

Example of Incremental Budgeting

Suppose a small business had a marketing budget of $50,000 in the previous year and intends to create an incremental budget for the upcoming year. After reviewing market conditions and the need to increase marketing efforts, they decide to allocate an additional 10% to the marketing budget. The incremental budget for marketing in the next year would be $55,000. This incremental adjustment accounts for expected changes in marketing costs and allows the business to plan for the upcoming period while building on the previous year’s financial plan.

How to Use Incremental Budgeting?

Using the incremental budgeting method involves a systematic approach to making adjustments to the previous budget to create a new financial plan. To implement incremental budgeting effectively, follow these steps:

1. Start with the Previous Budget: Begin by reviewing the previous year’s budget and its line items. Understand the allocations and spending patterns.

2. Identify Changes: Identify the factors that will impact the upcoming budget period. Consider inflation rates, changes in market conditions, business strategies, and departmental needs.

3. Analyze Cost Drivers: Determine the key cost drivers for each budget item. These are the factors that significantly influence expenses, such as labor costs, material costs, or production volumes.

4. Make Incremental Adjustments: Based on your analysis, make incremental adjustments to the budget. This can involve percentage increases or decreases, fixed-amount changes, or reallocations among departments.

5. Consult with Stakeholders: Seek input from relevant stakeholders, such as department heads, finance teams, or executives, to ensure alignment with organizational goals.

6. Review and Approve: Carefully review the adjusted budget to ensure it aligns with business objectives. Obtain necessary approvals to finalize the budget.

7. Implement and Monitor: Once approved, the incremental budget becomes the financial plan for the upcoming period. Continuously monitor actual spending against the budget to identify variances and take corrective actions when necessary.

Creating an Incremental Budget

Creating an incremental budget involves building on the previous year’s financial plan and making adjustments for anticipated changes. Start by gathering historical budget data and financial reports. Identify the key factors that will affect the budget, such as cost drivers and inflation rates. Then, incrementally adjust each line item based on these factors. Be sure to justify and document the reasons for each adjustment to provide transparency and accountability. Regularly review and update the budget throughout the fiscal year as new information becomes available and as business conditions change.

Incremental Budgeting Process

The incremental budgeting process typically consists of the following steps:

1. Analysis: Begin by analyzing the previous year’s budget and identifying the changes and factors that will affect the new budget period.

2. Adjustments: Make incremental adjustments to each line item in the budget based on the identified changes and cost drivers.

3. Stakeholder Input: Consult with relevant stakeholders, including department heads and finance teams, to gather input and validate the adjustments.

4. Review and Approval: Review the adjusted budget for accuracy and alignment with organizational goals. Seek approvals as needed.

5. Implementation: The approved incremental budget becomes the financial plan for the upcoming period. It serves as a guide for resource allocation and expenditure control.

6. Monitoring and Control: Continuously monitor actual spending against the budget and address any variances through corrective actions.

Using Incremental Budgeting Software

To streamline the incremental budgeting process, organizations can leverage budgeting and financial management software. These tools facilitate data analysis, adjustments, and tracking of incremental changes. They also provide visibility into the budgeting process, allowing stakeholders to collaborate effectively. Software solutions often include features for real-time monitoring, reporting, and scenario analysis, enhancing the accuracy and efficiency of incremental budgeting.

Comparing Incremental Budgeting with Other Budgeting Methods

Budgeting is a critical aspect of financial management, and different methods exist to create budgets. Two common approaches are incremental budgeting and zero-based budgeting.

Incremental Budgeting vs. Zero-Based Budgeting:

Incremental budgeting is a budgeting method that starts with the prior period’s budget as a baseline and makes incremental adjustments for the next period. It is often seen as the easiest budgeting approach since it involves minor changes to the current budget. In contrast, zero-based budgeting starts from scratch, requiring managers to justify every expenditure from the ground up.

Zero-based Budgeting is typically more time-consuming and involves a deeper level of analysis. While incremental budgeting is suitable for organizations that prefer stability and minor adjustments, zero-based budgeting is ideal when a thorough review of expenses is needed to identify potential cost savings or reallocate resources.

Advantages and Disadvantages of Incremental Budgeting

Incremental Budgeting Pros: The incremental budgeting method provides stability and continuity in financial planning. It is efficient and less time-consuming than some other budgeting methods since it builds upon the existing budget, making minor changes based on the previous period’s budget. This approach is particularly useful for organizations with relatively stable operations and when historical data is a reliable predictor of future expenses. Additionally, it requires less effort to implement compared to more comprehensive budgeting techniques.

Incremental Budgeting Cons: While incremental budgeting offers stability, it may lead to complacency and missed opportunities for cost savings or resource optimization. It assumes that the prior period’s budget is an accurate reflection of future needs, which may not always be the case, especially when changes in the business environment occur. Incremental budgeting can perpetuate inefficiencies and unnecessary expenses if not closely monitored and reviewed. Moreover, it may not be suitable for organizations that require a more dynamic and flexible budgeting approach to adapt to rapidly changing conditions.

Approach to Budgeting: Incremental vs. Zero-Based

The choice between incremental and zero-based budgeting depends on an organization’s specific needs, objectives, and the level of scrutiny required in financial planning. Incremental budgeting provides stability and is efficient for businesses with predictable expenses and minimal changes from year to year. In contrast, zero-based budgeting is a more rigorous approach that suits organizations seeking to challenge existing spending patterns, identify cost-saving opportunities, and allocate resources based on current needs and priorities. Each method has its advantages and disadvantages, and the decision should align with the organization’s financial management strategy and goals.

Common Issues with Incremental Budgeting

Incremental budgeting, while a commonly applied method, is not without its challenges. One common issue with this approach is the perpetuation of inefficiencies and unnecessary spending. Since incremental budgeting is based on past performance and previous budgets, it tends to assume that historical spending patterns are still valid, even if circumstances have changed.

This can lead to a lack of scrutiny in financial planning, making it challenging to identify and address potential cost-saving opportunities. Moreover, the incremental budgeting approach may allocate equal incremental changes to all budget items, regardless of their actual needs or priority. This can result in resources being misallocated and a failure to adapt to evolving business requirements.

Possible Pitfalls with Incremental Budgeting

Incremental budgeting is a straightforward budgeting process, but it has its pitfalls. One potential pitfall is the perpetuation of outdated or inefficient spending patterns. Since incremental budgeting is based on previous data and past performance, it may fail to adapt to changing business conditions or evolving priorities.

Additionally, this method may lead to budgetary slack, where departments or teams intentionally overestimate their budget needs to ensure they have sufficient resources. This can result in unnecessary spending and inefficiencies. To address these pitfalls, organizations using incremental budgeting should regularly review and analyze their budgets, challenge assumptions, and seek opportunities for cost optimization.

Addressing Budgetary Slack in Incremental Budgeting

Budgetary slack is a common issue in incremental budgeting, where departments or teams intentionally overestimate their budget needs to ensure they have a financial cushion. To address budgetary slack, organizations can implement measures such as setting stricter budget targets, encouraging transparent and accurate budget submissions, and conducting regular budget reviews. It’s essential to create a culture of accountability and align budgeting with performance targets to reduce the tendency for budgetary slack.

Dealing with Unnecessary Spending in Incremental Budgeting

Unnecessary spending can be a consequence of the incremental budgeting method. To mitigate this issue, organizations should conduct thorough budget reviews, challenging each budget item’s necessity and ensuring that expenditures align with current priorities and business objectives. Implementing cost control measures, such as regular expense tracking and analysis, can help identify and eliminate unnecessary spending. Additionally, organizations should foster a culture of cost-consciousness among employees to promote responsible budgeting practices and resource allocation.

Implementing Incremental Budgeting in Small Businesses

Small businesses can benefit from implementing incremental budgeting as it offers a straightforward and less resource-intensive approach to financial planning. For small businesses with limited financial management expertise, incremental budgeting is a suitable starting point. It involves making minor changes to the previous year’s budget, making it an accessible type of budgeting for those new to the process. Small businesses can use historical data as a foundation and allocate resources based on past performance, which can provide stability and help in financial planning.

Advantages for Small Businesses Using Incremental Budgeting

There are several advantages of incremental budgeting for small businesses. It is a relatively easy budgeting approach, making it well-suited for businesses new to budgeting. Small businesses can allocate resources based on the previous year’s budget with minor changes, reducing the complexity of the budgeting process. Incremental budgeting offers stability, as it maintains consistent funding for multiple years, which can be beneficial for small businesses with limited financial resources. Moreover, this approach allows small businesses to prioritize and allocate resources to key areas based on historical data, ensuring essential functions are adequately funded.

Challenges of Incremental Budgeting for Small Businesses

While incremental budgeting has advantages, it also presents challenges for small businesses. One major challenge is the potential for budgetary slack, where departments or teams may inflate their budget requests to secure additional resources. Small businesses must implement measures to encourage transparent and accurate budget submissions and conduct regular budget reviews to mitigate this issue. Additionally, relying solely on historical data may hinder adaptability to changing market conditions or business needs, which can pose challenges for small businesses aiming for growth and innovation.

Adjusting Incremental Budgeting for Small Business Needs

Small businesses can adjust incremental budgeting to better align with their specific needs. To address budgetary slack, they should establish clear budget targets and foster a culture of accountability. Small businesses can also introduce flexibility by allowing for incremental changes that respond to changing conditions or strategic priorities. This adaptability ensures that the budget remains relevant and effective for the business’s evolving needs.

How to Make Incremental Changes in Small Business Budgeting

Making incremental changes in small business budgeting involves a careful assessment of budget items to identify areas where adjustments are needed. Small businesses should conduct regular budget reviews to evaluate the performance and necessity of each budget item. Any changes should be aligned with the business’s strategic objectives and priorities, ensuring that resources are allocated optimally. This approach allows small businesses to maintain stability while making necessary adjustments to support growth and financial efficiency.

{kind=link}